Here's the 12-page deck that Ladder, a startup disrupting the 'crown jewel' of the insurance market, used to nab $100 million

Finance

Here’s the 12-page deck that Ladder, a startup disrupting the ‘crown jewel’ of the insurance market, used to nab $100 million

This story is available exclusively to Business Insider subscribers.

Become an Insider and start reading now.

Digital life-insurance startup Ladder just raised $100 million in Series D funding.

Backers include Thomvest Ventures and OMERS Growth Equity.

Ladder also announced that it has begun issuing its own policies directly.

Fintechs looking to transform how insurance policies are underwritten, issued, and experienced by customers have grown as new technology driven by digital trends and artificial intelligence shape the market.

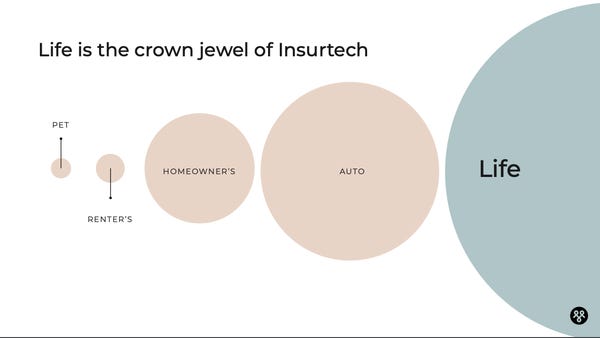

And while verticals like auto, homeowner’s, and renter’s insurance have seen their fair share of innovation from forward-thinking fintechs, one company has taken on the massive life-insurance market.

This story is available exclusively to Business Insider

subscribers.

Become an Insider

and start reading now.Have an account? .

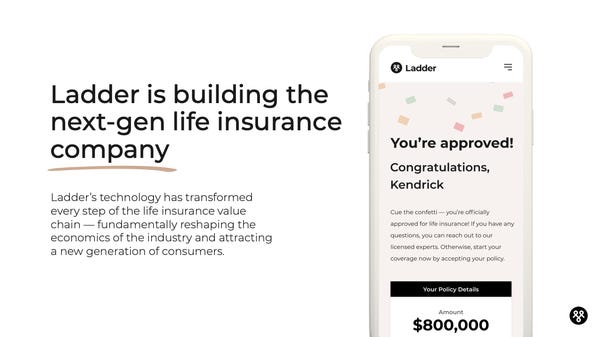

Founded in 2017, Ladder uses a tech-driven approach to offer life insurance with a digital, end-to-end service that it says is more flexible, faster, and cost-effective than incumbent players.

Life, annuity, and accident and health insurance within the US comprise a big chunk of the broader market. In 2020, premiums written on those policies totaled some $767 billion, compared to $144 billion for auto policies and $97 billion for homeowner’s insurance.

“It’s a product that funds the resilience of families and communities, which is good, but what’s amazing is that it is such a vast market that really, for a lot of reasons, has just under-invested in technology,” Jamie Hale, Ladder’s CEO and co-founder, told Insider.

On Monday, Ladder announced a $100 million, Series D fundraising led by Thomvest Ventures and OMERS Growth Equity.

Hale said the capital will be used to grow Ladder’s engineering team, primarily. Ladder currently has just under 100 employees, he added, with plans to roughly double that number over the next year.

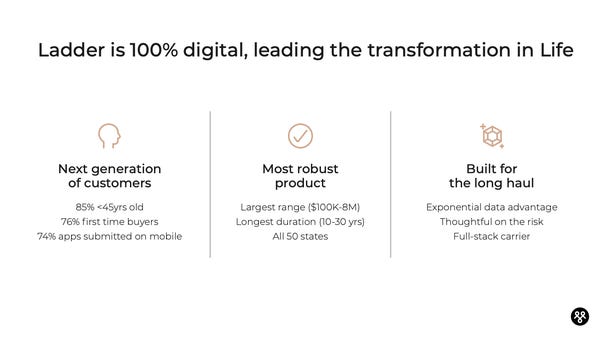

Ladder’s customers represent a younger, newer cohort of life-insurance buyers than those found at large incumbents, Hale said. About 75% of Ladder’s customers are first-time life-insurance buyers, he said, adding that the startup’s customers are, on average, about 15 years younger than those of incumbent players.

Together, the top-10 direct-issuing, individual life insurance companies control some 47% of the market, led by players like Northwestern Mutual, New York Life, and MassMutual, according to the Insurance Information Institute.

Directly issuing policies

Ladder also announced Monday that it issued its own policies for the first time through Ladder Life Insurance Company. It’s indicative of the startup’s goal to be fully vertically integrated within life insurance, one that Hale compared to neo-banks getting their own bank charters.

“What you’re going to see in insurtech overall is what you see in banking now and what you saw in payments to begin with. At first people come in and say, ‘Hey, I’m going to solve this really specific point problem. And as I solve that specific point problem, I see all the other problems around it, and in an way opportunity to re-engineer,'” Hale said.

Ladder now issues policies in two ways: Through partnerships with three other insurers — Fidelity Security Life Insurance, Allianz Life Insurance Company of New York, and Allianz Life Insurance Company of North America — as well as on its own. It’s a move that has seen Ladder gain approval to issue the policies in California, and Hale said the startup plans to seek licenses in other states in the future (unlike in banking, life insurance is nearly entirely regulated state by state).

Since inception, Hale said that $30 billion of policies had been written through Ladder’s service via its partners.

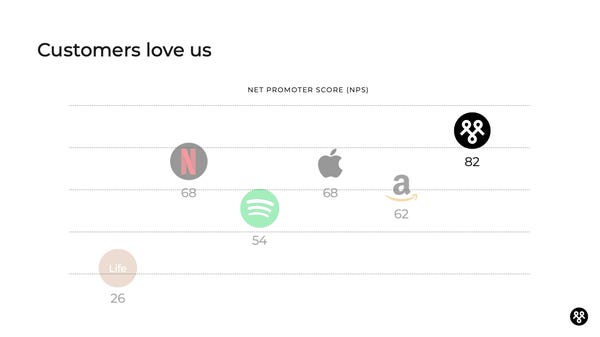

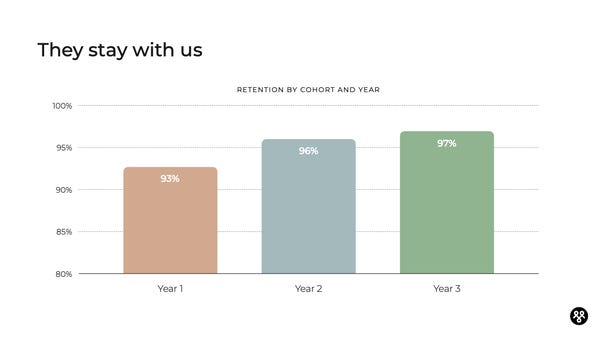

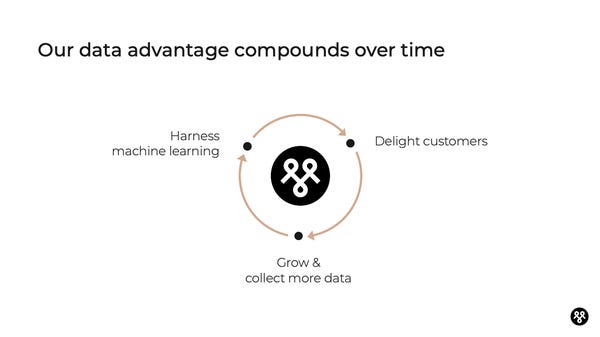

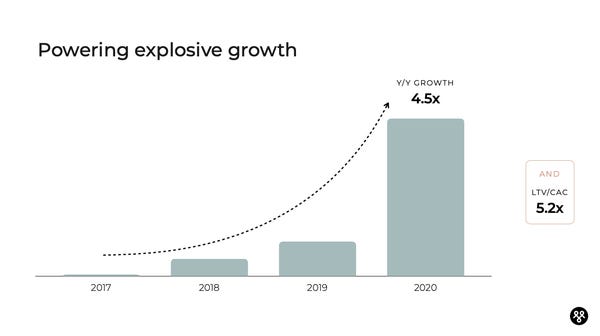

Here is the 12-page pitch deck Ladder used to raise the funds.